Understanding Medicare.. A Plain-Language Guide to Your Health Coverage Options

- Published By: shivaduvvuru

- April 24, 2026 / 10:37 AM IST

If you are approaching age 65 — or helping a family member navigate their health coverage — Medicare can seem confusing at first. This guide breaks it all down in plain, simple language. By the time you finish reading, you will understand what Medicare covers, what it does not, and how to protect yourself from big surprise bills.

Part 1: What Is Medicare?

Medicare is the federal government’s health insurance program for people who are 65 or older, as well as certain younger people with disabilities. Think of it like a basic health insurance plan paid for largely by taxes you and your employer contributed over your working years.

Original Medicare is made up of two main parts: Part A and Part B. Understanding both is the first step.

Medicare Part A — Hospital Insurance

Part A is sometimes called “hospital insurance.” It helps pay for care when you are admitted to a hospital, a skilled nursing facility (like a rehab center after surgery), or hospice care.

What Part A Covers:

• Inpatient hospital stays

• Skilled nursing facility care (after a qualifying hospital stay)

• Hospice care for the terminally ill

• Some home health care

What Part A Costs:

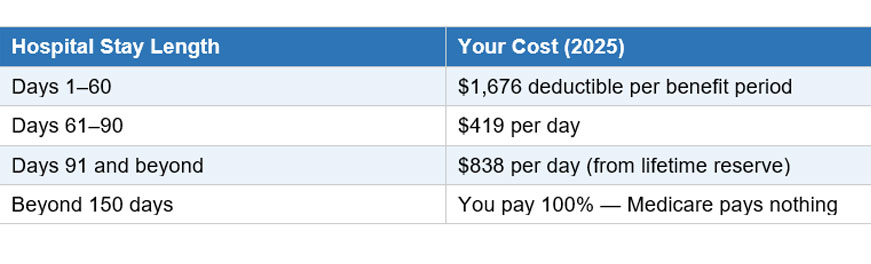

Most people do not pay a monthly premium for Part A because they (or their spouse) worked and paid Medicare taxes for at least 10 years. However, there are still out-of-pocket costs when you actually use it:

Key Point: A “benefit period” starts the day you are admitted to a hospital and ends when you have been out of the hospital for 60 days in a row. You could face the $1,676 deductible more than once in a year if you have multiple hospital stays.

Key Point: A “benefit period” starts the day you are admitted to a hospital and ends when you have been out of the hospital for 60 days in a row. You could face the $1,676 deductible more than once in a year if you have multiple hospital stays.

Medicare Part B — Medical Insurance

Part B is sometimes called “medical insurance.” It covers services you get outside of a hospital — doctor visits, lab tests, outpatient procedures, preventive care, and medical equipment like wheelchairs.

What Part B Covers:

• Doctor visits (primary care and specialists)

• Outpatient surgeries and procedures

• Lab tests and X-rays

• Preventive screenings (cancer screenings, flu shots, etc.)

• Mental health services

• Durable medical equipment (walkers, oxygen, etc.)

What Part B Costs:

• Standard premium: Monthly premium:

• Standard monthly premium: ~$185/month in 2025 (higher if your income is above certain limits)

• Annual deductible: ~$240/year

• After the deductible: You pay 20% of the approved cost for most services — with NO cap

Part 2: The Big Risk — The Uncapped 20%

This is the most important section in this entire guide. Please read it carefully.

With Original Medicare alone (no additional coverage), you are responsible for 20% of ALL Part B costs — forever, with no limit. This means if you have a serious illness or injury, your share of the bill could be enormous.

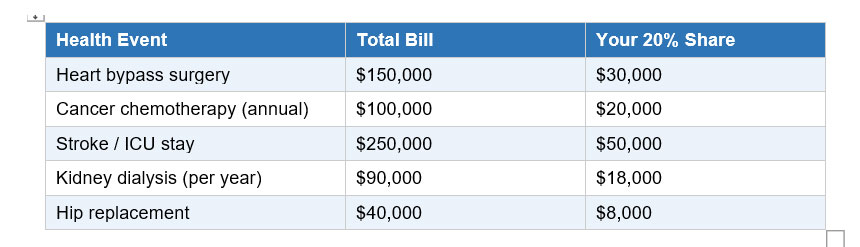

Real-World Example: You are diagnosed with cancer and your treatment costs $300,000. Medicare pays 80%, which is $240,000. You owe the remaining 20% — that is $60,000 out of your own pocket. And there is no cap. Ever.

Here Are More Examples of What 20% Could Mean:

These are not rare, extreme scenarios. Heart disease, cancer, and stroke are among the most common health events for people over 65. Without additional coverage, a single health event could drain your retirement savings.

This is precisely why most Medicare beneficiaries add either a Medicare Advantage plan or a Medigap (supplement) policy to their coverage — to protect themselves from this uncapped risk.

Employer Coverage: If you have health coverage through an employer, your employer plan may be your primary insurance and Medicare would be secondary — meaning your work plan pays first and Medicare picks up some of what is left. In this case you may not need Medigap or Advantage right away.

Part 3: Medicare Advantage Plans

Medicare Advantage (also called Part C) is an alternative way to get your Medicare coverage. Instead of Original Medicare paying your claims directly, you enroll in a private insurance plan that is approved by Medicare to provide your benefits.

Think of it like this: Medicare hands over your benefits to a private insurance company, which then manages your care.

What Medicare Advantage Plans Offer

• All the same benefits as Original Medicare Parts A and B

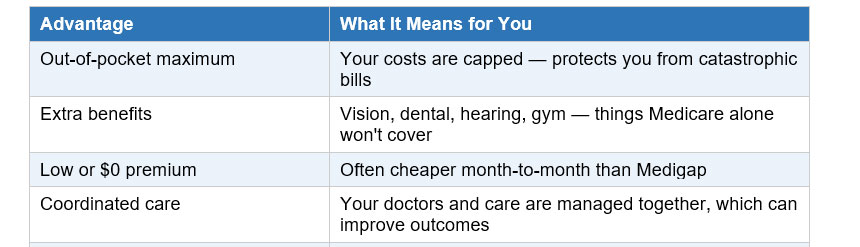

• A yearly out-of-pocket maximum (usually $8,850 or less in-network) — so the 20% risk IS capped

• Extra benefits Original Medicare does not cover, such as:

• Vision care (eye exams, glasses)

• Dental care (cleanings, X-rays, sometimes more)

• Hearing aids and exams

• Gym memberships and wellness programs

• Often has a $0 or low monthly premium (on top of what you still pay for Part B)

Advantages of Medicare Advantage

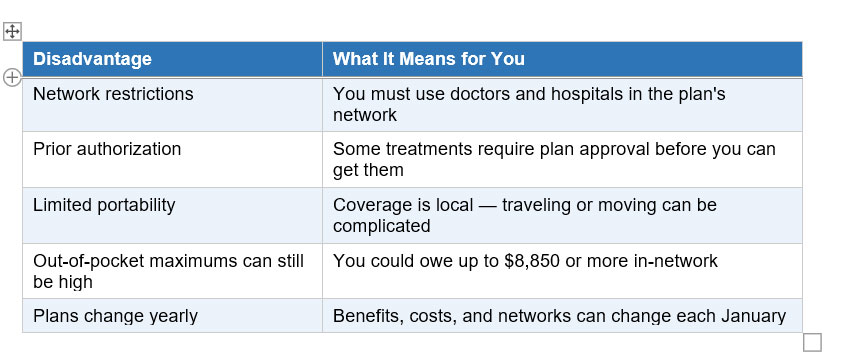

Disadvantages of Medicare Advantage

Important: If your doctor is not in the plan’s network, you may not be able to see them — or you may pay significantly more. Always check the network before enrolling.

Part 4: Medigap (Medicare Supplement) Plans

Medigap is not a replacement for Medicare — it works alongside Original Medicare to fill in the “gaps” in coverage. That is literally where the name comes from.

When you have a Medigap plan, Medicare pays its share first, then your Medigap policy pays most or all of what is left. The result: you pay very little out of pocket.

What Medigap Covers (Plan G — Most Popular)

• The Part B 20% coinsurance — fully covered

• The Part A hospital deductible ($1,676)

• Hospital coinsurance for days 61–90 ($419/day)

• 365 extra hospital days beyond what Medicare covers

• Part B excess charges (if a doctor charges more than Medicare allows)

• Emergency care during foreign travel (80% up to plan limits)

Bottom Line with Plan G: After your ~$240 Part B deductible each year, you essentially pay $0 for covered Medicare services — no matter how large the bill.

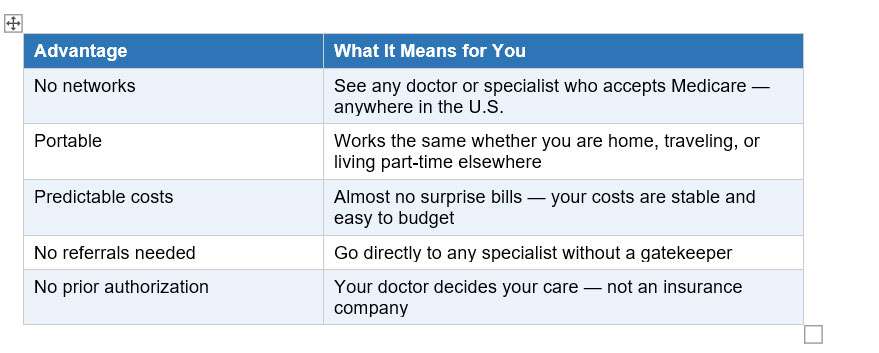

Advantages of Medigap

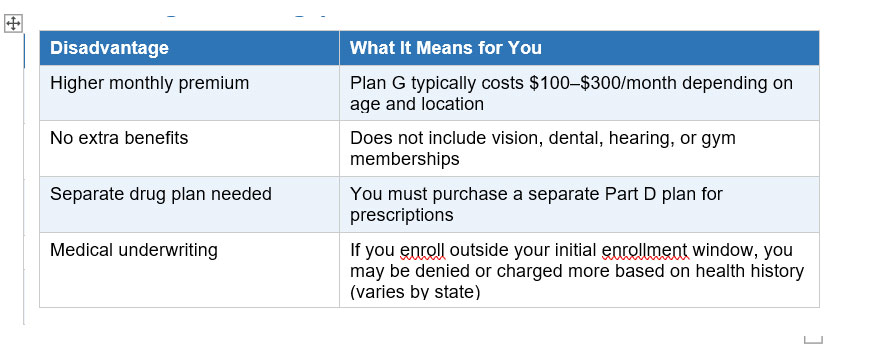

Disadvantages of Medigap

Part 5: Side-by-Side Comparison

The pros and cons of Medicare Advantage versus Medigap outlined above are accurate. Of all the factors to weigh, the toughest challenge with Advantage plans is the network — specifically, trying to keep the doctors you already know.

Conclusion: Which Option Is Right for You?

There is no single “best” answer — the right choice depends on your health, your doctors, your budget, and your lifestyle. But here are some general guidelines:

Consider Medicare Advantage if:

• You want extra benefits like dental, vision, hearing, and gym memberships

• You are comfortable staying within a network of doctors

• You want a lower monthly premium

• You do not travel frequently or spend time in multiple states

Consider Medigap if:

• You want the freedom to see any doctor without network restrictions

• You have ongoing relationships with specific doctors or specialists

• You want highly predictable, low out-of-pocket costs

• You travel frequently or spend time in different parts of the country

• You want the simplest, most comprehensive protection from the 20% risk

The most important takeaway: Do not rely on Original Medicare alone without any additional coverage. The uncapped 20% cost-sharing under Part B is a serious financial risk — one that could cost tens of thousands of dollars after a single major health event. Both Advantage plans and Medigap policies address this risk, each in their own way.

This article is for general educational purposes only and does not constitute personalized insurance or financial advice. Costs and plan details may change annually. Always consult a licensed Medicare advisor or the official Medicare.gov website for the most current information.