Big Screen, Bigger Picture: Inside India’s Pan-India Box Office and the Multiplex Betting On It

- Published By: techteam

- July 1, 2026 / 04:05 PM IST

The obituary for the Indian movie theatre has been written many times, usually by people watching something on their phones. The streaming surge was supposed to hollow out the multiplex. Instead, India just posted its biggest theatrical year ever, crossing ₹13,000 crore at the box office in 2025.

How that happened is the story of two forces feeding each other: a pan-India production model born in Telugu cinema and now reshaping Hindi cinema’s own economics and an exhibition business that has stopped fighting streaming on its own turf.

The Exhibitor’s View: Cinema as the Cultural Moment

Few people see the floor-level data more clearly than Devang Sampat, Managing Director of Cinépolis India, the country’s first international cinema exhibitor and one of its largest chains.

His framing is that streaming and cinema are not enemies competing for the same hours, but complementary formats serving different appetites. As he puts it: “OTT offers convenience and volume. Cinema offers something different the collective experience, the immersive environment, the cultural moment.” The conclusion he draws is simple and has held up: when the content is compelling enough, audiences still choose the theatre.

The behavioural data backs the nuance. Sampat notes that while moviegoing frequency has moderated since the pandemic—admissions are still running roughly 20% below pre-COVID levels audiences are making more deliberate, content-led trips, and increasingly on weekdays rather than only on big weekends. The job of the modern multiplex, in other words, is no longer to be there when a film releases. It’s to be worth the trip.

How “Pan-India” Rewrote the Economics

To understand why theatres are thriving, you have to understand the production shift that fills them. The phrase “pan-India” barely existed a decade ago, because the assumption was that only Hindi cinema could play nationwide. That assumption died in 2015 with S.S. Rajamouli’s Telugu epic Baahubali: The Beginning, and was buried by its 2017 sequel, RRR (2022), and finally Pushpa 2: The Rule (2024).

The model is now standard: build a spectacle big enough to travel, dub it into four or five languages, release everywhere at once, and treat the whole country plus the diaspora as a single market. Pushpa 2 ran on more than 12,000 screens worldwide, over 8,000 of them in India.

The most striking proof of the shift is hidden inside the Hindi numbers. Pushpa 2 was the highest-grossing film of 2024 at ₹1,403 crore gross and its Hindi dub alone collected ₹889 crore, making it the highest-grossing “Hindi” film of all time. A Hindi blockbuster that was never originally a Hindi film.

That isn’t a one-off. By Ormax’s accounting, roughly 31% of Hindi cinema’s 2024 collections (about ₹1,464 crore) came from dubbed versions of South Indian films. Strip those dubs out, and original Hindi-language films actually fell about 37% year on year, from roughly ₹5,085 crore in 2023 to ₹3,215 crore in 2024. Bollywood’s headline numbers are increasingly propped up by South Indian content wearing a Hindi voice.

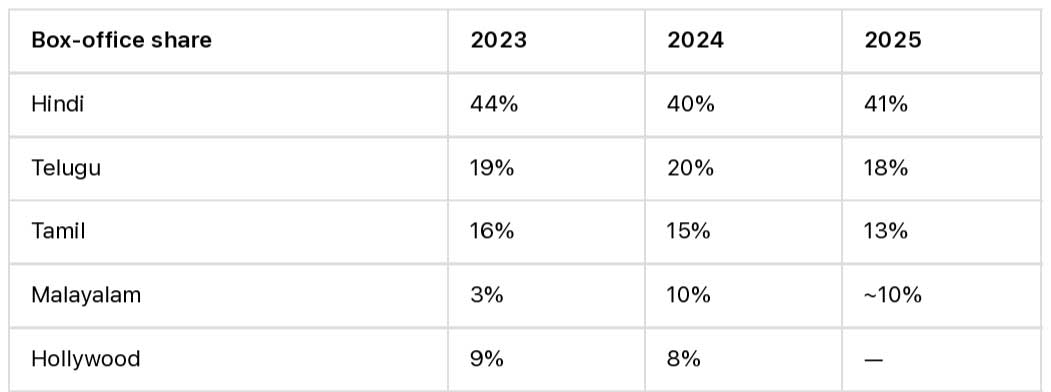

The Numbers: 2023–2025 The last three years tell the story better than any narrative. First, how the pie split by language:

Two things stand out. Hindi never actually lost the top spot in share terms it dipped in 2024 and reclaimed its footing in 2025 with its best-ever year, around ₹5,504 crore, powered by Chhaava and Saiyaara. And the real mover of the period was Malayalam, which roughly tripled its share on a run of disciplined mid-budget hits, crossing ₹1,000 crore for the first time.

But look at the South collectively and the balance of power is clearer: in 2024, South Indian cinema took in around ₹5,646 crore roughly 20% more than Hindi cinema’s ₹4,679 crore. The “regions” are no longer a sideshow to Bollywood; together they are the main event.

Now Telugu cinema on its own, and the tension that defines its present:

Revenue crept up every year while footfalls fell every year. That gap is the whole picture in two rows: Tollywood’s growth since 2023 was bought with higher ticket prices, not bigger crowds roughly six crore fewer Telugu tickets sold in 2025 than in 2023, yet collections still edged to a record.

The Pan-India Illusion:

The danger in all of this is believing the label is a guarantee. It isn’t. Trade voices now argue that being hailed as pan-India and being pan-India are different things a true pan-Indian film performs in every circuit, and only a handful of names reliably command that pull: Prabhas, Allu Arjun, Yash, and director Rajamouli.

The cautionary tales are recent. Ram Charan’s Game Changer (2025) reportedly recovered less than a third of its enormous budget. Jr. NTR’s Devara held at home in Telangana but dropped sharply around 70%in northern markets within its first week. Spectacle ambition is a high-variance bet; a blockbuster in one language does not automatically become a hit across the country.

Cinépolis’s Bet: More Screens, Smarter Economics

This is the backdrop against which exhibitors are expanding not despite the volatility, but because of the structural headroom underneath it. India remains one of the most underscreened large markets in the world, and Sampat sees that low screen density as the opportunity.

His growth plan, on a base of close to 500 screens, runs along a few lines:

Screen expansion. Around 40 new screens a year roughly 10% annual growth split between direct investment (about 20) and a Franchise-Owned, Company-Operated model (about 20), where developers carry 70–90% of the build cost. Each screen runs to roughly ₹3 crore.

Catchment over tiers. Rather than a metro-versus-small-town strategy, Cinépolis evaluates a 5–7 km catchment radius, betting that proximity and mall quality matter more than city size. Some metros still have untapped pockets; some smaller cities are already saturated.

Value-led pricing. Average ticket price growth is deliberately kept below inflation, to protect cinema’s status as accessible mass entertainment.

Beyond the ticket. Food and beverage is targeted to rise from roughly 50% of box office today toward 70–75%, while advertising already growing well ahead of box office becomes a bigger pillar via the chain’s digital “Spotlight” network.

Filling the weekdays. With weekend crowds near saturation for the biggest films, the growth lever is converting slow weekday slots into steady admissions.

The Real Picture:

Put it together and the “death of cinema” narrative looks exactly backwards. Streaming didn’t kill the theatre; it clarified its job. The pan-India model didn’t dethrone Bollywood so much as end the idea that any one industry sits on the throne alone Hindi still leads on share, the South leads collectively, and Malayalam keeps overperforming its size.

India’s box office is now genuinely multipolar, structurally under-penetrated, and growing. The film most likely to top the all-India charts next year could come from Hyderabad, Chennai, Bengaluru, Kochi, or Mumbai and whichever city it comes from, the multiplex is betting it can sell the one thing a phone can’t: the room full of strangers, all gasping at once.

Related News

From Budget Rooms to a Global Booking Empire: The Ritesh Agarwal Story

Maruti Suzuki Collaborates with Five Startups for Innovation and Efficiency

HDFC Bank Parivartan Launches 12 Community Development Initiatives in Telangana

Print Expo and Media Expo 2026 Expand to Their Largest Editions

Bandhan Large Cap Fund Celebrating Two Decades of Stability and Growth